Italian economy: employment is ok, GDP isn't. Recession in Europe and America slows down.

by Fabrizio Galimberti and Luca Paolazzi

Why the discrepancy between a weak economy and strong employment?

FASTEN YOUR SEATBELTS

"Ladies and Gentlemen, this is the captain speaking. We have begun our descent and will be landing soon. Please fasten your seat belts..." The plane of the world economy is decreasing in altitude and losing speed, in the hope of landing on the runway of more sustainable growth, i.e. in line with potential and without inflation or deflation.

The markets are betting on a soft landing without any accidents. In fact, the probability of dying in a plane crash is almost four times lower than that of being eaten by a shark (David Ropeik, Harvard University, 2006). It is well-known, however, that 70% of plane crashes take place during this delicate stage of the flight.

However, it is an outdated statistic, because it refers to a time when many aircraft were not equipped with a ground proximity sensor.

The problem with the economy is that this type of sensor does not exist, simply because we don't even know what altitude the ground is at, i.e. the potential rate of growth that we have to aim for. Or rather, the econometric estimates of this growth certainly do exist and are made seriously, but they are valid for a medium-long period of time; whereas in the "here and now", this growth may have moved up or down depending on the context: historical, social, technological, political and - as we discovered in 2020 - healthcare.

Furthermore, there are so many sources of turbulence, starting with various wars, unfortunately, where air pockets and jolts are guaranteed. We remain confident in the pilots' expertise, despite being forced by circumstances to navigate by sight. However, it would be best to fasten your seat belts tightly.

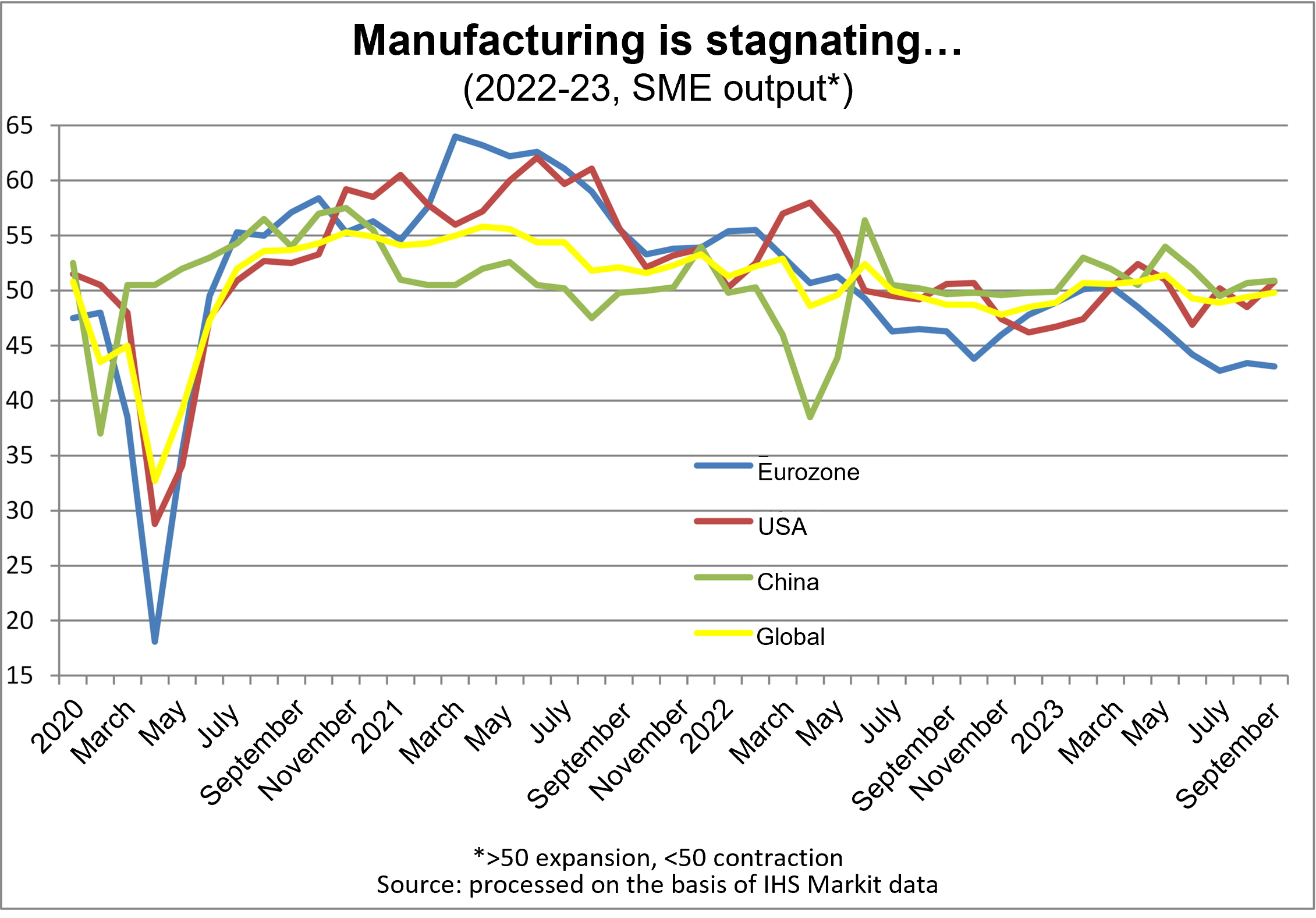

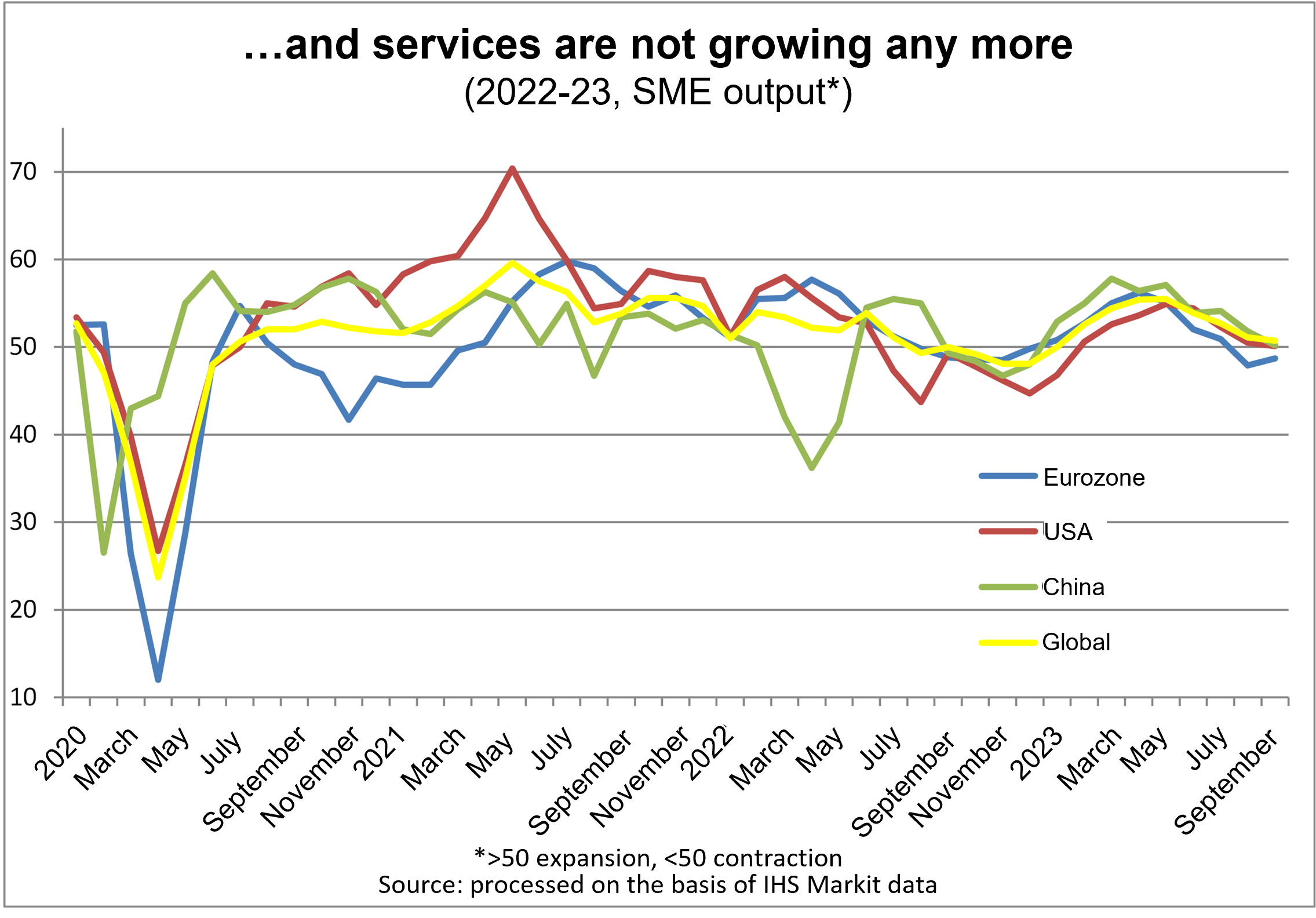

In fact, the cyclical indicators of global orders and production say that the engines have stalled to a dangerous extent, even running backwards; in fact, orders globally are contracting, especially those from abroad. This decline is being caused by manufacturing orders, which are more sensitive to the "diet" imposed by monetary policy (capital assets and durable goods, in particular) and to the geopolitical tensions that are redrawing the map of production locations and international trade. Orders for services, on the other hand, are flat.

SME production figures show the geographical mix of the situation and what we can see is that the alarm bells are ringing louder in one sense and softer in another. The mitigation derives from the observation that output is not falling. It has only stopped increasing, with the composite SME index at 50, poised between rising and falling. But the trend is downwards, as in an inexorable countdown: from 54.4 in May, every month has shown a reduction in speed.

The increase in alarm derives precisely from geographical diversification: the Eurozone has clearly been in recession for some time now according to this qualitative data, since June to be precise, and in October it took a further step down, in the sense that the contraction accelerated. What is keeping GDP a little higher is the contribution being made by the public sector, whose services and spending at least do not go down, just as they do not add any impetus when the economy picks up.

The trend of orders in the Eurozone is still on the decline, indeed they are falling at the highest rate since September 2012 in the midst of a sovereign debt crisis (excluding the tragic parenthesis of the pandemic). So we have to expect further dips in activity.

Also because many companies have started to reduce their workforce, albeit softly softly (by not replacing those who leave), and after 32 consecutive months of increases, the total number of employees has remained stable overall. This removes the sort of parachute that always supported European economic systems up to now, making them particularly resilient to the hammer blows of interest rate hikes suffered on the anvil of the rising cost of living. Before looking into what is happening in the European labour market, let's look at other areas of the world.

The first thing we have to take note of is that after the extraordinary exploit of the third quarter (GDP up by +4.9% on an annualised basis), the USA is now on course for a much slimmer, but still robust, 2.1% in the fourth quarter. Employment continues to rise, and not even much slower: including the 30,000-plus workers on strike in the auto industry (which US statistics do not include among those who are working), employed people in the three months to October rose by 1.7% on an annualised basis, in line with what has been happening since April. An increase that is consistent with the number of vacancies, which is still high, being equal to 1.5 times the number of unemployed people in September, a ratio that has remained substantially unchanged since July.

US consumer perception is also still clearly in favour of an abundance of job opportunities ("plentiful" beats "hard to get" 3 to 1), so their confidence level remains high and incompatible with lower spending. However, few analysts realise that this shortage of workers was already apparent before the pandemic; so much so that since the beginning of 2018 there have been more jobs available than the number of workers ready to fill them, and this is more and more the case. This explains the tension in the American labour market and how pressures to increase wages will persist. We'll return to this topic later on when we talk about inflation. And in any case, demand is held up by strong public spending, directly or via subsidies, in investments to modernise infrastructure and to apply the slogan "Make America great again!".

Turning to the East, we can see China going zigzag and Japan weakening, while India is growing at a slightly less robust pace and the other economies in the area are suffering from global manufacturing difficulties. Russia is a story of its own: a war economy at the gallop, circumventing sanctions thanks to the complicity of the rest of the world outside of the USA and Europe; in fact, not so much "the rest", as they are the vast majority!

In short, the picture is one of weakness with a black hole, the Eurozone, and a star that is still shining, the USA. This is another reason why trying to achieve a soft landing is more laborious and dangerous.

Returning to the Old Continent, in addition to the famous jobless recovery, as in the period after the 2001 recession in America, like many learned explanations of this phenomenon, in the current phase the economic bestiary offers a new surprise: the jobful recession; in other words, an economy that weakens, while employment continues to rise strongly.

As we have complained on various occasions, employment statistics in the Eurozone are very poor on a monthly level, being limited only to unemployment. Which rose slightly in September after reaching an all-time, historical low (in the short history of the Eurozone) in August. While the quarterly figures confirm that GDP has not moved for four consecutive quarters, companies are continuing to look for employees, and employment has increased. In any case, the creation of new jobs in the private sector came to an end in October. And in Italy?

In the Bel Paese, the "odd couple" of a year of stagnant GDP and rising employment goes to the extreme, because the number of new hires went up by 2.2%: more than half a million people.

THE ITALIAN JOB-MACHINE

What is happening? There are various explanations: a change of mix towards activities with a lower level of productivity; underestimation of the dynamics of GDP; employment as a delayed indicator (like the light we can see from dead stars); the need for businesses to top up their workforce.

The truth is probably a mix of all four: recently, the main driver has come from the services that revolve around travel and tourism; it wouldn't be the first time that GDP ought to be revised upwards; it takes some time before the fall in demand and production leads to a decline in the number of people who are employed. Like their European, US, Japanese and Australian counterparts, Italian companies have had to refuse orders due to lack of staff. Now they are building up their strength in preparation for the recovery.

Fact is that on both sides of the Atlantic the resilience of the labour market is acting as a stabiliser of the plane as it lands.

THE NRRP AS A LIFEJACKET

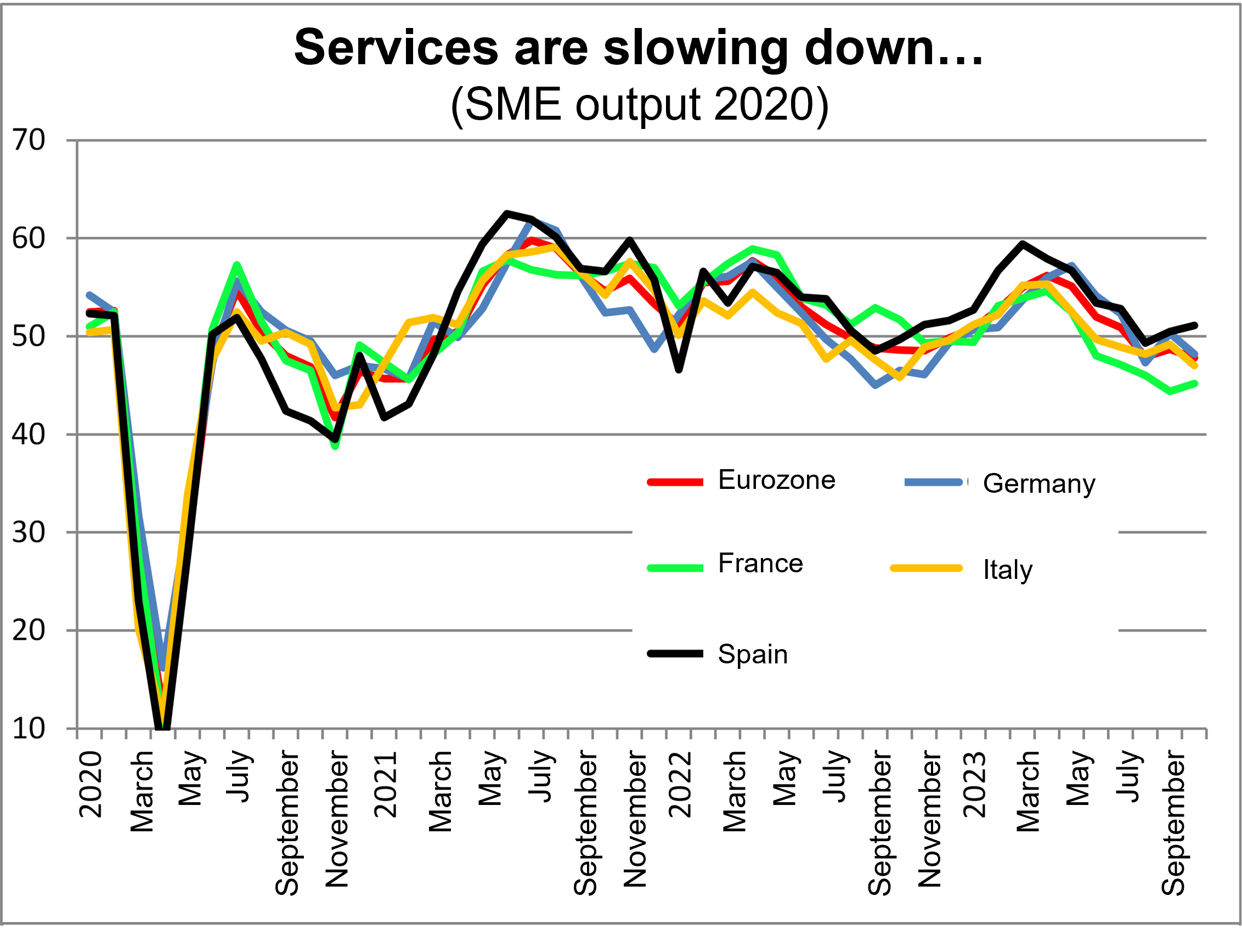

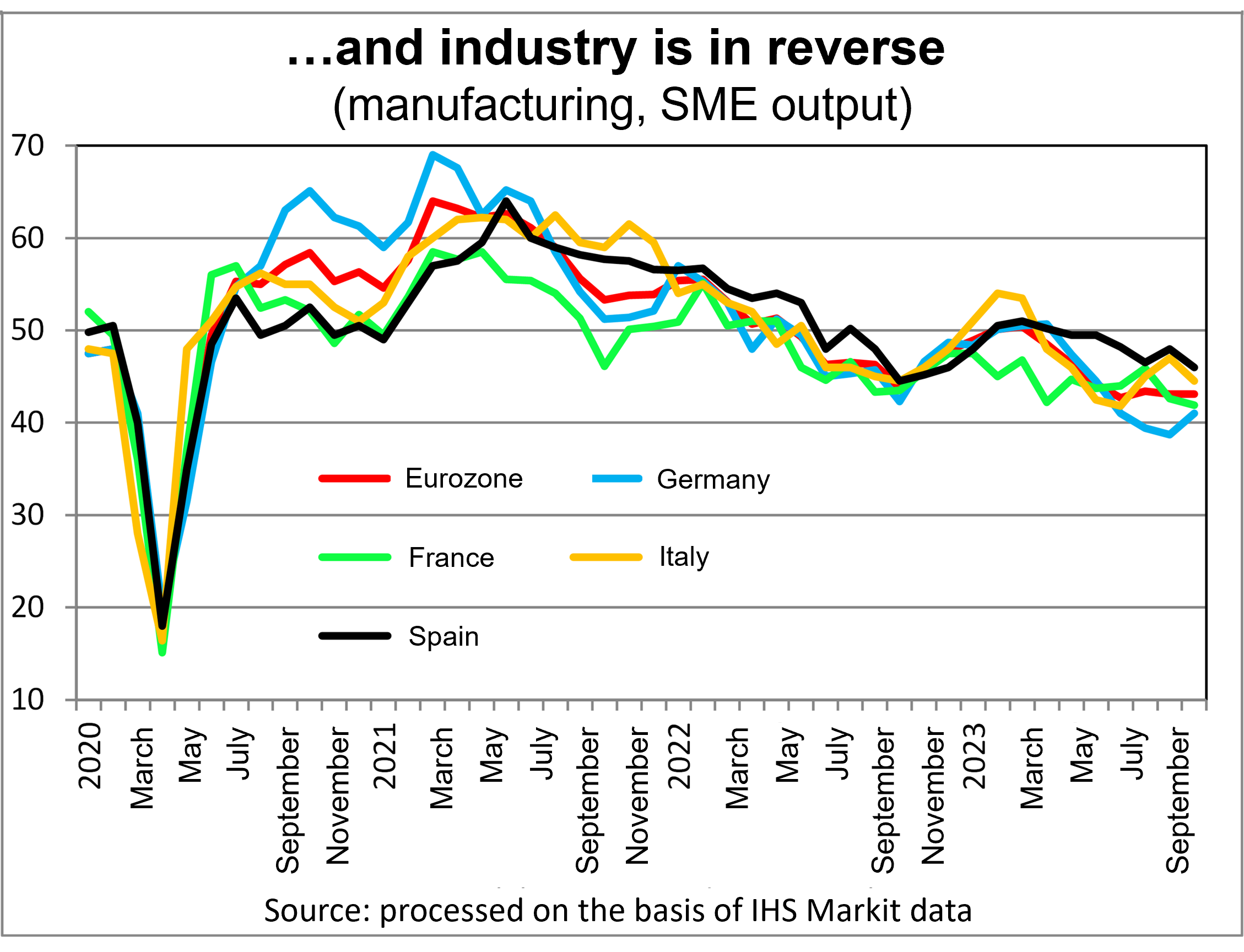

However, the economic trend says that production in the fourth quarter began to contract more violently across the Eurozone, with the exception of Spain (SME composite output).

For once, Italy seems to be doing better than France and Germany. It is not reporting any difficulties of his own, but that is slim consolation. Also because the government's budget proposals raise the deficit, but do not create much more growth. Once again, we would emphasise that we have a massive lifejacket in the form of the NRRP.

________________________________________________________________________________________________________________________________________________

Fabrizio Galimberti was born in Rome in 1941. After graduating from the Bocconi University in Milan, he studied at Columbia University in New York, and subsequently taught Public Economics in Rome and Ferrara. Later he worked at the OECD Economics Department. In Rome, he was an economic advisor to the Treasury, with Beniamino Andreatta and Giovanni Goria. In later years, he was FIAT Chief Economist and most recently a leader writer with Il Sole 24 Ore.